In our previous post about driving Health Savings Account (HSA) adoption, we covered how to mitigate employee risk with your health plan design. In this final post in our series, we’ll focus on employee HSA education. HSA survey respondents who cited a “lack of employee understanding” (51%) had lower HSA adoption rates.

- Step 1: Seed Early Adopters

- Step 2: Find Your Employer Contribution Sweet Spot

- Step 3: Mitigate Employee Risk with Your Plan Design

- Step 4: Educate Employees

Two tactics can be applied to encourage HSA uptake:

- Apply the theory of loss aversion in your messaging.

- Describe an HSA as a “medical 401(k)”—before you introduce the health plan.

Apply the Theory of Loss Aversion

You may have encountered the study of behavioral economics and the theory of loss aversion. In a nutshell, it says when people make a decision, they are motivated more by fear of loss than what they stand to gain.

Reframe your messaging to show the dollar value of what’s being lost by not using an HSA. This is more impactful than showing what’s being gained. You’re trying to encourage employees to try something new and step outside of the familiarity of a traditional PPO. Start by demonstrating the true cost of a traditional PPO.

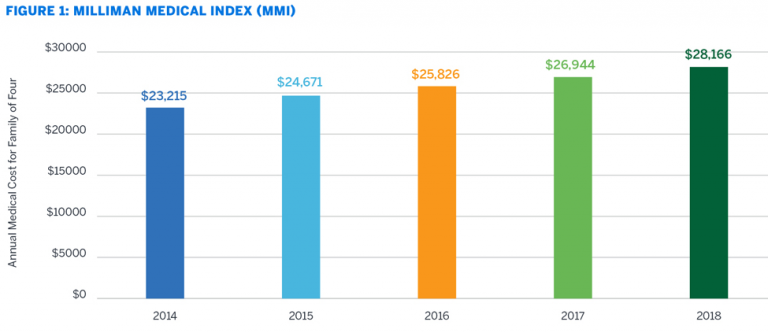

In 2018, a typical family on a PPO will spend $28,166 on healthcare.

According to the 2018 Milliman Medical Index (MMI), the health care cost this year for a typical family of four on an employer-sponsored PPO is $28,166.  Most employees don’t realize how much their PPO premiums impact their take-home salary (just like most don’t know how much their employer contributes to their health care plan premiums).

Most employees don’t realize how much their PPO premiums impact their take-home salary (just like most don’t know how much their employer contributes to their health care plan premiums).

Premiums are sunk costs.

Help employees dimension their annual healthcare costs compared to their medical needs. Here’s one way to talk about it:

- Premiums are paid to the insurance carrier.

- Traditional PPOs come with a hefty monthly premium.

- A lower premium provides the opportunity to put the difference in a personal savings account.

Once you’ve laid the groundwork, you can introduce Health Savings Accounts using familiar language.

Describe an HSA as a “Medical 401(k)”

Health Savings Accounts have always had a branding problem. To start with, HSAs are often confused with FSAs. Add to this that you have to explain another confusing and bad-sounding term, high-deductible health plan (HDHP) before you can even get into what an HSA is. It’s a complicated acronym stew. Because of this, when we heard a practical explanation during Lumity’s market research on the 2018 State of the HSA, we took note. Jason Cabrera, Benefits Manager, US, Shutterstock, told us, “I explain HSAs like having a medical 401(k) you can dip into now to pay for qualified medical, dental, or vision expenses not covered by your plan—or, you can let it build to pay for qualified health expenses after you retire.” Lumity now uses this analogy when explaining HSAs, and it really resonates with our clients’ employees.

Talk about the HSA first, not the plan.

Start by leveraging the familiar concept of a 401(k). If you ask employees to think of an HSA like a medical 401(k), it lays a common frame of reference. And you can talk about the HSA first—before getting into the added complexity of explaining how a high-deductible health plan factors in.

7 HSA Talking Points

- Like a 401(k), the money is yours to keep even if you change employers or insurance.

- Use it to pay for qualified medical, dental, or vision expenses now, or—even better—let your savings build for future use.

- An HSA complements a 401(k) to bolster your retirement savings—HSA funds can be used in retirement to pay for qualified medical expenses.

- Any employer contribution is free money.

- There’s a triple tax advantage:

- Contributions to an HSA are not federally taxed;

- Funds in an HSA grow tax-free; and

- Funds used to pay for qualified medical expenses are not taxed. (Most state laws treat HSAs similarly, but there are exceptions).

- If your HSA administrator provides the option to invest—point this out. (Not all HSAs are equal. Some HSA administrators only offer HSAs as savings accounts with minimal interest rates).

- At a certain balance, you’re able to invest HSA dollars into mutual funds similar to a 401(k) or IRA

- Doing so increases your long-term earning potential

- The best part? Any capital gains your HSA funds earn are also tax-free

- HSAs can also be combined with a Limited Purpose FSA or Dependent Care FSA (we’ll save this topic for a future article).

Because HSA funds can be used to pay medical bills at any time, it can be a good strategy to max out contributions to an HSA first, at the beginning of a plan year, then focus on maxing out a 401(k).

Show real-world examples.

It can be encouraging to point to real-world examples of people just getting started with an HSA. For inspiration, check out the 20somethingfinance blog articles by G.E. Miller:

- HDHP vs. PPO, Costs, Savings, & Thoughts: After the Switch

- Reach Health Insurance Nirvana with an HDHP & HSA

Even for older-than-20-somethings, the examples hold up.

Now onto Explaining the Health Plan

After you’ve seeded interest in an HSA, you can introduce the requirement for a Consumer Driven Health Plan (CDHP), also known as a High-Deductible Health Plan (HDHP). Doing so makes it easier to dimension how an HSA pairs with the plan to reduce out-of-pocket costs. Regarding plan education, Jason Cabrera also offered these insights:

I tend to stay away from the ‘HDHP’ acronym. I find that using ‘Consumer Driven Health Plan’, or CDHP, lends itself to the real purpose of this type of health plan—consumerism. It is easily argued that Americans spend more on healthcare per capita than any other country on the planet. Coupling this with traditional healthcare plans can lead to unnecessary overuse which, in turn, affect insurers and employers. By promoting consumerism, the focus shifts from ‘using it because my co-pay is only $X for an office visit’ to ‘Do I really need to see my doctor for a sore throat the first day it’s sore?’ By offering a lower premium, the employee can set aside the premium cost savings into their HSA and choose when they think it’s best to seek medical attention.

We’ll follow Jason’s lead as we frame the plan’s talking points.

6 CDHP Talking Points

- A high-deductible means a low monthly premium (which means less money deducted from your salary).

- The tradeoff is you cover 100% of the costs, including prescriptions—until you hit your deductible, then insurance kicks in.

- While this may sound scary, remember you’re getting a discounted rate on these services, or the “contracted rate,” simply by having the CDHP.

- It’s worth pointing out that CDHPs typically cover 100% of the following medical expenses regardless of where you stand with your deductible:

- All well-child visits (1, 2, 4, 6, 9, 12, 15, 18, and 24 months of age)—these can add up!

- One wellness visit per year per adult

- Flu shots as well as a list of preventative care services for men and women, like prostate exams and mammograms

- Make sure you use in-network doctors and providers.

- This significantly reduces your out-of-pocket expenses, and

- It ensures any costs you incur are applied towards your deductible.

- Remember—your HSA funds can be used to pay for medical, dental, or vision expenses not covered by your plan. This offsets your out-of-pocket costs.

- If you’re worried about a worst-case medical scenario, high-deductible health plans have a maximum out-of-pocket cost.

- This maximum represents your total financial exposure. (But, depending on your company’s plan design, even hitting the max on a CDHP can still cost less than using a PPO).

In essence, with a CDHP, what employees spend on health care aligns more closely with their medical needs—they’re no longer overpaying. Year after year, the savings can add up.

Moving forward

As healthcare costs continue to rise, HSAs will remain a powerful tool for reducing expenses for both employers and employees. This is a wrap to our 4-part series. If you’d like to know how your HSA strategy or plan design measures up, contact Lumity for a complimentary consultation. We’ll benchmark your situation, and you’ll learn how you compare to other companies in your industry and region.